Navigating the complex world of college financing can feel like deciphering a secret code, but understanding subsidized loans is one of the most crucial keys to unlocking affordable higher education. These federal student loans represent a significant opportunity for students to reduce the long-term cost of their degrees, offering terms that are far more favorable than most other borrowing options. For many, they are the cornerstone of a financially sound college plan, directly impacting how much debt they'll carry into their post-graduation lives.

In an era where the cost of college continues to rise, making informed decisions about how to fund your education is more critical than ever. While various financial aid options exist, federal student loans, particularly direct subsidized loans, stand out due to their unique benefits designed to support students with demonstrated financial need. This comprehensive guide will demystify subsidized loans, outlining their advantages, eligibility requirements, and how they stack up against other loan types, ensuring you're equipped to make the best choices for your academic and financial future.

Table of Contents

- Understanding Subsidized Loans: The Basics

- Eligibility: Do You Qualify for Subsidized Loans?

- The Core Advantage: Interest-Free Periods

- Subsidized vs. Unsubsidized Loans: A Crucial Comparison

- Federal Direct Subsidized Loan Limits for Undergraduates

- Why Subsidized Loans Should Be Your First Choice

- Navigating the Application Process: Your FAFSA Guide

- Managing Your Subsidized Loans: Repayment and Beyond

Understanding Subsidized Loans: The Basics

When discussing financial aid for higher education, the term "subsidized loans" frequently comes up, and for good reason. A direct subsidized loan is a type of federal student loan, specifically made through the William D. Ford Federal Direct Loan Program, where a borrower isn’t generally responsible for paying interest during certain periods. This crucial benefit sets them apart from almost all other forms of borrowing for education. These loans are designed to help undergraduate students who have a demonstrated financial need, a determination made by the information provided on your Free Application for Federal Student Aid (FAFSA).

The federal government, through the Department of Education, offers these loans directly to college students. The "subsidized" aspect means that the interest that would normally accrue on the loan while you are enrolled in school at least half-time, during your grace period (typically six months after you leave school), or during periods of deferment (when payments are temporarily paused) is paid by the government. This effectively means your loan balance doesn't grow during these critical times, leading to significant cost savings over the life of the loan. For any student looking to minimize their borrowing costs, understanding and prioritizing these loans is paramount.

Eligibility: Do You Qualify for Subsidized Loans?

Unlike some other federal loan types, subsidized loans come with a specific set of eligibility criteria, primarily centered around financial need. You must show financial need to qualify for subsidized loans. This need is not simply about whether you can afford tuition out-of-pocket, but rather a calculation performed by the Department of Education based on your FAFSA information, comparing your Expected Family Contribution (EFC) with the cost of attendance at your chosen institution. The lower your EFC, the higher your demonstrated financial need, and thus, the more likely you are to qualify for these beneficial loans.

To qualify for a subsidized loan, also called a direct subsidized loan, you have to fill out the Free Application for Federal Student Aid (FAFSA). This application is the gateway to virtually all federal student aid, including grants, work-study, and federal loans. Beyond demonstrating financial need, students must also meet other general eligibility requirements for federal student aid, such as being a U.S. citizen or eligible non-citizen, being enrolled at least half-time in an eligible program at an eligible school, and maintaining satisfactory academic progress (SAP) as defined by your college or university. Failing to meet SAP can result in the loss of federal aid eligibility, including your subsidized loans, so staying on top of your grades and credits is essential.

The Core Advantage: Interest-Free Periods

The most compelling benefit of direct subsidized loans lies in their unique interest subsidy. As mentioned, a borrower isn’t generally responsible for paying interest on these loans during specific periods. This isn't just a minor perk; it's a game-changer for student borrowers. Imagine taking out a loan where the interest doesn't pile up while you're focused on your studies. That's precisely what subsidized loans offer.

Specifically, the federal government covers the interest that accrues on your subsidized loan:

- While you are enrolled in school at least half-time.

- During your grace period, which is typically the six months after you graduate, leave school, or drop below half-time enrollment.

- During periods of deferment, which are approved times when you can temporarily postpone your loan payments due to specific circumstances, such as unemployment or economic hardship.

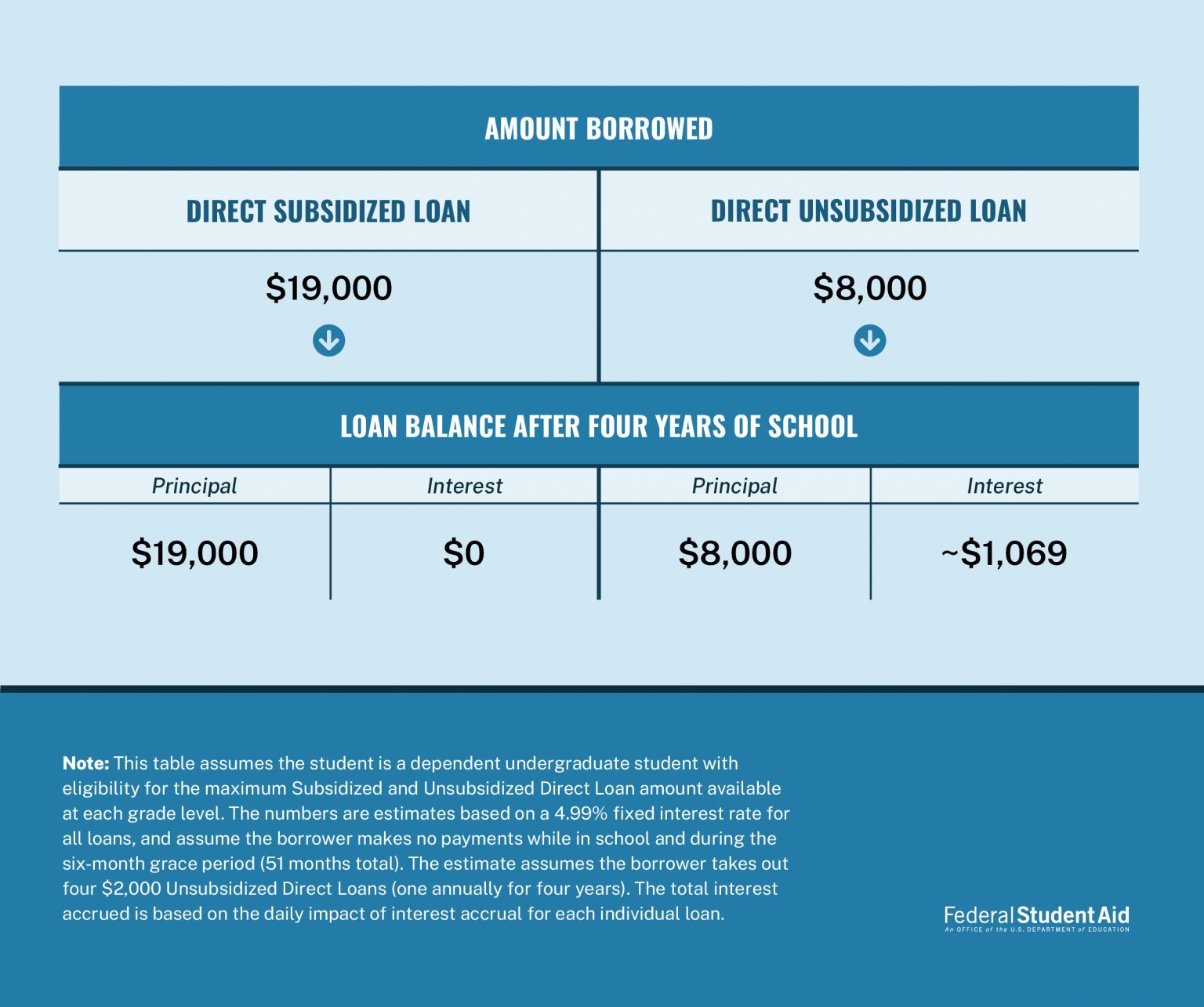

This feature directly translates into significant cost savings. For unsubsidized student loans, interest begins accruing immediately after the loan is disbursed, even while you're still in school. This means that by the time you graduate, the principal amount you borrowed has already grown due to accumulated interest. With subsidized loans, your principal balance remains exactly what you borrowed until your repayment period begins. This difference can save students hundreds, if not thousands, of dollars over the life of their loan, making the overall cost of their education much more manageable. It's a clear illustration of why, if you qualify, you should always maximize your subsidized loan eligibility first.

Subsidized vs. Unsubsidized Loans: A Crucial Comparison

When considering federal student loans to pay for school, the first loan types you should consider are federal direct subsidized and unsubsidized loans. While both are offered by the federal government and have generally favorable terms compared to private loans, these two federal loan types differ in key aspects that can significantly impact your overall borrowing cost. Understanding these differences is paramount to making informed decisions about financing your education. We review the difference between subsidized vs. unsubsidized student loans, including eligibility, loan limits, and interest rates.

Eligibility Differences

The most fundamental distinction lies in eligibility. As previously discussed, direct subsidized loans are exclusively for undergraduate students who demonstrate financial need. This means your family's income and assets play a role in determining if you qualify. Unsubsidized loans, on the other hand, are available to both undergraduate and graduate students, and eligibility is not based on financial need. This makes them more widely accessible, but they lack the crucial interest subsidy benefit. While unsubsidized loans are a valuable option, particularly for those who don't qualify for subsidized aid or need additional funds, they should always be considered after maximizing your subsidized loan eligibility.

Interest Accrual Differences

This is where the true cost savings of subsidized loans become apparent. With a direct subsidized loan, the Department of Education pays the interest while you are in school at least half-time, during your grace period, and during periods of deferment. This means your loan balance does not grow during these times. Conversely, interest on unsubsidized loans begins to accrue immediately after the loan is disbursed. While you are not required to make payments on unsubsidized loans while in school, the interest will continue to accumulate. If you don't pay this interest as it accrues, it will be capitalized (added to your principal balance) when repayment begins, leading to a larger loan amount and more interest paid over time. This capitalization can significantly increase the total cost of your education, which is why you should always consider the cost savings you get with subsidized loans.

Loan Limits and Terms

Both subsidized and unsubsidized loans have annual and aggregate (total) borrowing limits, but these limits can vary based on your dependency status and year in school. Subsidized loans generally have better terms, but eligibility is stricter, and the annual limits are typically lower than those for unsubsidized loans. For instance, while an independent undergraduate student might be able to borrow up to $12,500 annually in a combination of subsidized and unsubsidized loans, the subsidized portion would be capped at a lower amount. The interest rates for both types of federal direct loans are fixed for the life of the loan and are generally set by Congress each year. While the rates are the same for both subsidized and unsubsidized loans for a given academic year, the interest subsidy on subsidized loans makes their effective cost much lower.

Federal Direct Subsidized Loan Limits for Undergraduates

Understanding the specific borrowing limits for subsidized loans is essential for effective financial planning. The amounts you can borrow annually are determined by your year in school and whether you are a dependent or independent student. For undergraduates, these limits are set to ensure students borrow responsibly while still having access to necessary funds.

Undergraduates may borrow up to $3,500 for the first year. For the second year, this limit increases to $4,500. For third-year and beyond undergraduates, the annual limit for subsidized loans typically remains at $5,500. These are annual limits, meaning the maximum amount you can receive in subsidized loans during a single academic year. It's important to note that these limits are part of your overall federal direct loan eligibility. For example, if your subsidized loan eligibility is $3,500 for your first year, and you need more funds, you might then be offered unsubsidized loans up to your total annual federal loan limit.

Beyond annual limits, there are also aggregate limits, which represent the total amount of federal student loans you can borrow over your entire academic career. For dependent undergraduate students, the aggregate limit for subsidized loans is $23,000. This means that even if you qualify for the maximum annual amount each year, you cannot exceed $23,000 in total subsidized loans throughout your undergraduate studies. For independent undergraduate students (or dependent students whose parents are unable to obtain a PLUS loan), the aggregate limit for subsidized loans remains $23,000, but their overall federal direct loan limit (including unsubsidized loans) is higher. These limits are in place to prevent excessive borrowing and encourage responsible financial management, ensuring that students do not accumulate an unmanageable amount of debt.

Why Subsidized Loans Should Be Your First Choice

If you need student loans to pay for school, the first loan types you should consider are federal direct subsidized and unsubsidized loans. This isn't just a suggestion; it's a fundamental principle of smart financial aid planning. The reasons are clear and compelling, rooted in the unique benefits that these federal loans, particularly the subsidized variety, offer compared to private loans or even other forms of federal aid.

Firstly, the interest subsidy is an unparalleled advantage. No private loan, and no other federal loan type (except for certain specific programs like Perkins Loans, which are no longer widely available), offers the benefit of the government paying your interest while you're in school or during periods of deferment. This directly translates to significant cost savings. When you consider the cost savings you get with subsidized loans, it's evident that they minimize the amount you'll owe upon graduation, making your repayment journey much more manageable. Avoiding interest accrual for several years can save you hundreds, if not thousands, of dollars over the life of your loan.

Secondly, federal loans generally come with more flexible repayment options and borrower protections than private loans. This includes income-driven repayment plans, which adjust your monthly payments based on your income and family size, and opportunities for deferment or forbearance if you face financial hardship. These safety nets are rarely, if ever, offered by private lenders. While unsubsidized loans also share these benefits, the interest subsidy of subsidized loans makes them the superior option if you qualify. Prioritizing subsidized loans ensures you're accessing the most favorable terms available, laying a strong foundation for your financial well-being after graduation.

Navigating the Application Process: Your FAFSA Guide

The gateway to accessing subsidized loans, and indeed most federal student aid, is the Free Application for Federal Student Aid (FAFSA). This form is absolutely crucial for any student seeking financial assistance for college. To qualify for a subsidized loan, also called a direct subsidized loan, you have to fill out the Free Application for Federal Student Aid (FAFSA) every year you plan to attend college.

The FAFSA collects detailed financial information about you (and your parents, if you are a dependent student) to determine your Expected Family Contribution (EFC) and, subsequently, your financial need. This EFC is then used by colleges to calculate your eligibility for various types of aid, including subsidized loans, unsubsidized loans, grants, and work-study programs. It's important to complete the FAFSA as early as possible each year, as some aid is awarded on a first-come, first-served basis, and deadlines vary by state and institution. The FAFSA typically opens on October 1st for the following academic year.

The process involves gathering necessary documents like tax returns, W-2 forms, and bank statements. While it might seem daunting, there are many resources available to help, including online guides, school financial aid offices, and even a FAFSA helpline. Accuracy is key when filling out the FAFSA, as errors can delay your aid package or lead to incorrect aid offers. Remember, the FAFSA is free to complete; you should never pay a service to help you fill it out. By diligently completing your FAFSA each year, you ensure that you are considered for all federal aid opportunities, including the highly advantageous subsidized loans, setting yourself up for the most affordable college experience possible.

Managing Your Subsidized Loans: Repayment and Beyond

Securing subsidized loans is a fantastic first step, but understanding how to manage them throughout your academic career and into repayment is equally vital. While the federal government covers interest during certain periods, these are still loans that must eventually be repaid. Proactive management can significantly impact your financial health post-graduation.

Once you graduate, leave school, or drop below half-time enrollment, your subsidized loans enter a grace period, typically lasting six months. During this time, you are not required to make payments, and the interest continues to be subsidized. This period is designed to give you time to find employment and prepare for repayment. It's a critical window to start planning your repayment strategy. You'll be assigned a loan servicer, who will be your point of contact for all repayment-related matters. They will provide information on your loan balance, interest rate, and available repayment plans.

The federal student loan program offers various repayment plans, including standard, graduated, extended, and several income-driven repayment (IDR) plans. IDR plans are particularly beneficial if you have a lower income after graduation, as they cap your monthly payments at a percentage of your discretionary income and can even lead to loan forgiveness after 20 or 25 years of qualifying payments. Understanding these options and choosing the plan that best fits your financial situation is crucial. Furthermore, if you encounter financial hardship, options like deferment and forbearance can temporarily pause your payments, though interest may accrue on unsubsidized portions of your loans during these periods. For subsidized loans, interest continues to be covered during approved deferments. By staying informed, communicating with your loan servicer, and making timely payments, you can successfully manage your subsidized loans and pave the way for a strong financial future.

In conclusion, direct subsidized loans stand out as one of the most valuable forms of financial aid available to college students. Their unique interest subsidy, coupled with flexible repayment options and borrower protections, makes them an indispensable tool for funding higher education without accumulating excessive debt. By understanding their eligibility requirements, diligently completing the FAFSA, and recognizing their distinct advantages over unsubsidized and private loans, students can make truly informed decisions about their financial future.

The journey through college finance can be complex, but armed with the knowledge about subsidized loans, you are better positioned to make choices that will save you money and reduce stress. Don't leave money on the table; always prioritize these beneficial federal loans. Have you applied for your FAFSA yet? What are your biggest concerns about student loan repayment? Share your thoughts in the comments below, or explore more of our articles on financial aid strategies to further empower your educational journey!

Related Resources:

Detail Author:

- Name : Tyler Braun

- Username : jules12

- Email : qhoppe@hotmail.com

- Birthdate : 1982-11-16

- Address : 2849 Lucie Lock New Austyn, ND 32968-4337

- Phone : 331.901.3018

- Company : Cormier-Gutmann

- Job : Taper

- Bio : Aliquam sed ut deleniti. Aut velit ut aut ea numquam. Asperiores mollitia at dolorum praesentium neque perferendis.

Socials

twitter:

- url : https://twitter.com/malloryking

- username : malloryking

- bio : Illo omnis ullam sint et nisi. Qui ut corporis quia voluptas quam. Nostrum aspernatur illum dignissimos accusamus accusantium assumenda.

- followers : 5791

- following : 1002

facebook:

- url : https://facebook.com/malloryking

- username : malloryking

- bio : Error perferendis mollitia quisquam atque eveniet reiciendis non.

- followers : 3256

- following : 1707