**Navigating the complex world of student financial aid can feel like deciphering a foreign language, especially when terms like "subsidized" and "unsubsidized" loans enter the conversation. Yet, understanding the fundamental differences between these two primary types of federal student loans is not just beneficial; it's absolutely crucial for making informed decisions that will impact your financial well-being for years to come.** These choices directly influence how much you pay in interest, when that interest begins to accrue, and ultimately, the total cost of your education. For many aspiring students, federal student loans are an indispensable tool for funding higher education. However, not all loans are created equal, and knowing the nuances of each option can save you thousands of dollars over the life of your loan. This comprehensive guide will demystify subsidized vs unsubsidized loans, providing you with the knowledge needed to choose the best loan option for your unique financial situation. --- **Table of Contents:** 1. [Understanding Federal Student Loans: The Foundation](#understanding-federal-student-loans-the-foundation) 2. [Subsidized Loans: The Need-Based Advantage](#subsidized-loans-the-need-based-advantage) * [Eligibility for Subsidized Loans](#eligibility-for-subsidized-loans) * [Interest Accrual and Government Subsidy](#interest-accrual-and-government-subsidy) * [Borrowing Limits for Subsidized Loans](#borrowing-limits-for-subsidized-loans) 3. [Unsubsidized Loans: Broader Access, Immediate Interest](#unsubsidized-loans-broader-access-immediate-interest) * [Eligibility for Unsubsidized Loans](#eligibility-for-unsubsidized-loans) * [Interest Accrual on Unsubsidized Loans](#interest-accrual-on-unsubsidized-loans) * [Borrowing Limits for Unsubsidized Loans](#borrowing-limits-for-unsubsidized-loans) 4. [Key Differences at a Glance: Subsidized vs Unsubsidized Loans](#key-differences-at-a-glance-subsidized-vs-unsubsidized-loans) 5. [Interest Rates and Repayment Terms: What You Need to Know](#interest-rates-and-repayment-terms-what-you-need-to-know) 6. [Choosing the Best Loan Option for You](#choosing-the-best-loan-option-for-you) 7. [Application Process and Repayment Strategies](#application-process-and-repayment-strategies) 8. [Maximizing Your Financial Aid Strategy](#maximizing-your-financial-aid-strategy) ---

Understanding Federal Student Loans: The Foundation

When considering financial aid options for higher education, the first loans you should consider are federal direct subsidized and unsubsidized loans. Both subsidized and unsubsidized are part of the federal student loan program, meaning they come directly from the U.S. Department of Education. This is a significant advantage over private loans, as federal loans typically offer more favorable terms, including fixed interest rates, income-driven repayment plans, and opportunities for deferment or forbearance in times of financial hardship. They also don't require a credit check for most borrowers, making them accessible to a wider range of students. Understanding these foundational aspects is key before diving into the specific differences between subsidized vs unsubsidized loans.Subsidized Loans: The Need-Based Advantage

Direct Subsidized Loans are often considered the most advantageous type of federal student loan because the government pays the interest that accrues while you are in school at least half-time, during your grace period (the six months after you leave school), and during periods of deferment. This unique benefit can lead to significant cost savings over the life of the loan. To qualify for subsidized loans, students must demonstrate financial need. This is a crucial distinction that sets them apart from their unsubsidized counterparts.Eligibility for Subsidized Loans

The primary criterion for Direct Subsidized Loans is demonstrated financial need, as determined by the information provided on your Free Application for Federal Student Aid (FAFSA). Generally, only undergraduate students are eligible for these loans. This means that if you are pursuing a graduate or professional degree, you will not qualify for a Direct Subsidized Loan, regardless of your financial situation. This focus on undergraduate financial need ensures that the students who require the most assistance to cover their educational costs receive the benefit of interest subsidy.Interest Accrual and Government Subsidy

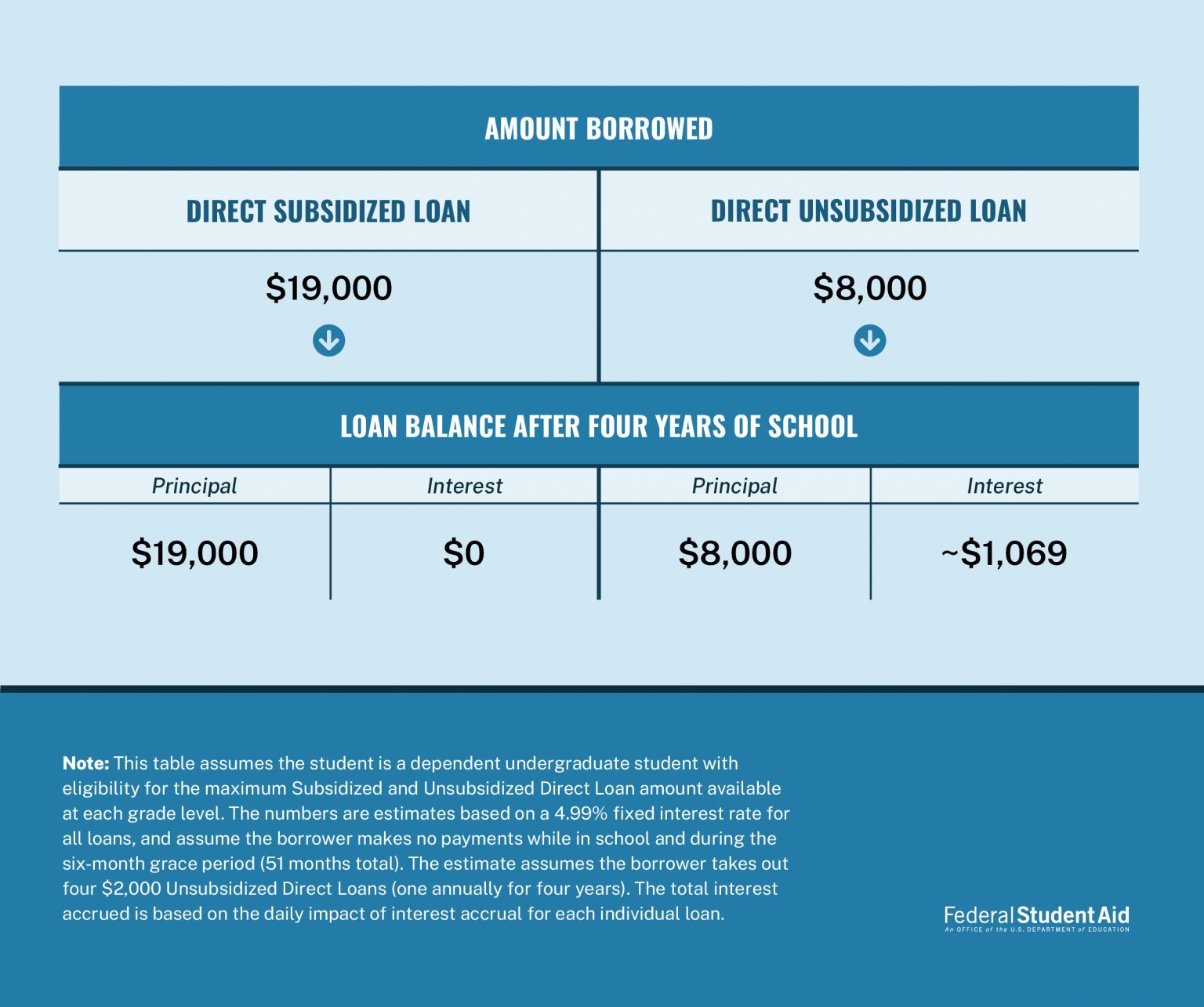

The big difference between subsidized and unsubsidized loans is when interest starts accruing on your federal student loans. For subsidized loans, the government pays the interest while you are enrolled in school at least half-time, during your grace period, and during any periods of deferment. This means that the loan amount you borrow is the exact amount you owe when you enter repayment, assuming you haven't made any payments during those periods. This interest rate subsidy provided by the government is a powerful benefit, as it prevents your loan balance from growing larger while you are still in school or experiencing temporary financial difficulties. When looking at subsidized vs unsubsidized student loans, consider the cost savings you get with subsidized loans due to this feature.Borrowing Limits for Subsidized Loans

There are specific annual and aggregate borrowing limits for Direct Subsidized Loans, which vary based on your dependency status and year in school. For undergraduates, these limits are generally lower than those for unsubsidized loans. For instance, undergraduates may borrow up to $3,500 for the first year, $4,500 for the second year, and $5,500 for subsequent years, with an aggregate limit of $23,000 for dependent students. Independent students have higher aggregate limits, but the annual subsidized limits remain the same. These limits are set to ensure that the most financially needy students receive support, but not to an extent that encourages over-borrowing.Unsubsidized Loans: Broader Access, Immediate Interest

Direct Unsubsidized Loans are available to a broader range of students because they do not require a demonstration of financial need. This makes them a viable option for virtually all students pursuing higher education, from undergraduates to graduate and professional students. While they offer more flexibility in terms of eligibility, they come with a crucial difference regarding interest accrual that borrowers must understand.Eligibility for Unsubsidized Loans

Unlike subsidized loans, unsubsidized loans do not require students to demonstrate financial need. This means that nearly any student enrolled at least half-time in an eligible program can qualify for a Direct Unsubsidized Loan, regardless of their family's income or assets. This broader eligibility extends to both undergraduate and graduate students, making them a common choice for those who do not qualify for subsidized loans or who need to borrow more than their subsidized loan limits allow.Interest Accrual on Unsubsidized Loans

Here lies the most significant difference when comparing subsidized vs unsubsidized loans: interest starts accumulating from the moment the unsubsidized loan is disbursed. This means that interest begins to accrue while you are in school, during your grace period, and during any periods of deferment or forbearance. If you choose not to pay the interest while it's accruing, it will be capitalized (added to your principal balance) when you enter repayment. This increases the total amount you owe and the total interest you'll pay over the life of the loan. Understanding this immediate interest accrual is vital for managing the overall cost of your education.Borrowing Limits for Unsubsidized Loans

Direct Unsubsidized Loans generally have higher annual and aggregate borrowing limits compared to subsidized loans. These limits also vary by your dependency status and academic level. For example, dependent undergraduate students can borrow up to $5,500 for their first year (with a maximum of $3,500 in subsidized loans), and independent undergraduates can borrow up to $9,500 for their first year. Graduate and professional students can borrow significantly more, up to $20,500 annually, with an aggregate limit of $138,500 (including any undergraduate loans). These higher limits acknowledge that many students, particularly at the graduate level, will need to borrow more to cover their educational expenses.Key Differences at a Glance: Subsidized vs Unsubsidized Loans

To truly grasp the distinctions, let's learn the differences between subsidized and unsubsidized federal student loans, such such as interest rates, borrowing limits, and eligibility, in a concise comparison: * **Eligibility:** * **Subsidized:** Requires demonstrated financial need. Only for undergraduate students. * **Unsubsidized:** No financial need required. Available to undergraduate and graduate students. * **Interest Accrual:** * **Subsidized:** Government pays interest while you're in school (at least half-time), during grace periods, and during deferment. * **Unsubsidized:** Interest starts accumulating from the moment the loan is disbursed. You are responsible for all interest. * **Borrowing Limits:** * **Subsidized:** Lower annual and aggregate limits, specifically for undergraduates. * **Unsubsidized:** Higher annual and aggregate limits, for both undergraduates and graduates. * **Cost Savings:** * **Subsidized:** Offers significant cost savings because interest doesn't accrue while you're in school or during grace/deferment periods. * **Unsubsidized:** Can be more expensive overall if interest is allowed to capitalize, as it adds to the principal balance. Understanding these key differences between subsidized vs unsubsidized student loans is paramount for making an informed decision on financing your education. The big difference between subsidized and unsubsidized loans is when interest starts accruing on your federal student loans, directly impacting your total repayment amount.Interest Rates and Repayment Terms: What You Need to Know

While the eligibility and interest accrual mechanics differ, the actual interest rates and repayment terms are often quite similar for both subsidized and unsubsidized federal direct loans. Federal student loan interest rates are set annually by Congress and are fixed for the life of the loan. For loans first disbursed between July 1, 2025, and June 30, 2026, Direct Subsidized and Unsubsidized Loans for undergraduates have the same interest rate, which is 6.39 percent. Direct Unsubsidized Loans for graduate and professional students typically have a slightly higher interest rate. It's worth noting that until July 1, 2008, the interest rate for unsubsidized loans was the same as for the subsidized loan, but on or after July 1, 2008, rates began to differentiate more consistently based on loan type and borrower level. Repayment terms are largely the same as for the federal subsidized loan. Both loan types typically enter repayment six months after you graduate, leave school, or drop below half-time enrollment. Federal loans offer a variety of repayment plans, including: * **Standard Repayment Plan:** Fixed monthly payments over 10 years. * **Graduated Repayment Plan:** Payments start low and increase every two years, over 10 years. * **Extended Repayment Plan:** Fixed or graduated payments over up to 25 years for higher loan balances. * **Income-Driven Repayment (IDR) Plans:** Payments are based on your income and family size, with any remaining balance forgiven after 20 or 25 years of payments. These flexible repayment options are a major benefit of federal loans, providing a safety net for borrowers who may struggle to make payments after graduation.Choosing the Best Loan Option for You

When looking at subsidized vs unsubsidized student loans, you might be wondering which is better. The answer is straightforward: if you need student loans to pay for school, the first loans you should consider are federal direct subsidized loans. Subsidized loans generally have better terms, primarily due to the government paying your interest while you're in school. You must show financial need to qualify for subsidized loans, so if you're eligible, always accept the full amount of subsidized loans offered to you before considering unsubsidized options. Once you've exhausted your subsidized loan eligibility, or if you don't qualify for them, Direct Unsubsidized Loans are the next best option among federal loans. While interest accrues immediately, the fixed interest rates and flexible repayment options still make them preferable to most private student loans. Only after exploring all federal loan options should you consider private student loans. Compare rates, terms, and benefits of private student loans from various lenders, but be aware that they often come with variable interest rates, fewer borrower protections, and require a strong credit history or a co-signer. Ultimately, to choose the best loan option for your financial situation, you need to assess your financial need, your academic level, and your comfort level with interest accruing while you're still in school. Find out how to choose the best loan option for your specific circumstances by prioritizing subsidized loans, then unsubsidized, and only then exploring private alternatives.Application Process and Repayment Strategies

The application process for both subsidized and unsubsidized federal loans begins with completing the Free Application for Federal Student Aid (FAFSA). This form determines your eligibility for all types of federal financial aid, including grants, work-study, and both types of Direct Loans. Your school's financial aid office will then use the information from your FAFSA to determine your financial need and the types and amounts of federal loans you qualify for. They will then send you an award letter outlining your financial aid package. Once you've accepted your loans, it's crucial to understand how they affect your interest and repayment. For unsubsidized loans, even though payments aren't due until after you leave school, consider making interest-only payments while you're enrolled. This proactive approach can prevent interest capitalization and significantly reduce the total amount you repay. For both loan types, familiarize yourself with the various repayment plans available. Learn how subsidized and unsubsidized loans differ in eligibility, interest, and repayment options, and use this knowledge to compare the pros and cons of each type of federal student loan and find out which one is better for you.Maximizing Your Financial Aid Strategy

Beyond simply understanding subsidized vs unsubsidized loans, a holistic approach to financing your education involves maximizing all available financial aid. This means: * **Applying for Scholarships and Grants:** These are forms of "free money" that do not need to be repaid. Pursue as many scholarship opportunities as possible, both through your school and external organizations. * **Considering Work-Study:** If offered, federal work-study programs allow you to earn money to help pay for educational expenses, reducing your reliance on loans. * **Borrowing Only What You Need:** While it can be tempting to borrow the maximum amount offered, only take out what is absolutely necessary to cover your educational and living expenses. Every dollar you borrow is a dollar you'll have to repay, plus interest. * **Budgeting Effectively:** Create a detailed budget to track your expenses and ensure you're living within your means. This can help minimize the amount you need to borrow. By combining a smart borrowing strategy for subsidized and unsubsidized federal loans with other forms of aid and responsible financial habits, you can significantly reduce your student loan debt and set yourself up for a stronger financial future. --- In conclusion, the journey through higher education is a significant investment, and how you choose to finance it can have lasting repercussions. Learning the differences between subsidized and unsubsidized federal loans, how they affect your interest and repayment, and how to choose the best option for you is a critical step in becoming a financially literate student. Both subsidized and unsubsidized loans are valuable components of the federal student aid program, offering distinct benefits and considerations. By prioritizing subsidized loans, understanding the immediate interest accrual of unsubsidized loans, and exploring all your financial aid options, you can make informed decisions that pave the way for academic success and a healthier financial future. We hope this guide has illuminated the distinctions between subsidized vs unsubsidized loans. Do you have any personal experiences with these loan types, or perhaps a question we didn't cover? Share your thoughts in the comments below! And if you found this article helpful, consider sharing it with friends or family who might also benefit from understanding these crucial financial aid options.Related Resources:

Detail Author:

- Name : Katelynn Prohaska

- Username : lea.purdy

- Email : joshuah64@gmail.com

- Birthdate : 1995-10-10

- Address : 22896 Steve Groves Apt. 050 Beierland, IL 12679-4539

- Phone : (254) 346-6369

- Company : Jerde LLC

- Job : Rough Carpenter

- Bio : Voluptatibus ullam reprehenderit excepturi laudantium. Sint quibusdam consequatur quasi optio non et. Modi incidunt distinctio minima. Vel et qui ab consequatur vitae at.

Socials

twitter:

- url : https://twitter.com/diego_id

- username : diego_id

- bio : Possimus asperiores quis odio et non. Et quia atque officiis nemo qui et officiis dolorem. Magnam qui illo suscipit illo dolores cupiditate velit.

- followers : 390

- following : 2407

instagram:

- url : https://instagram.com/dgoodwin

- username : dgoodwin

- bio : Dolorem accusamus amet impedit saepe. At voluptatem est sunt pariatur odit.

- followers : 5291

- following : 480

tiktok:

- url : https://tiktok.com/@diego.goodwin

- username : diego.goodwin

- bio : Qui vitae ratione debitis optio. Qui laudantium sapiente facere amet quis.

- followers : 2938

- following : 98

linkedin:

- url : https://linkedin.com/in/goodwin1971

- username : goodwin1971

- bio : Est repudiandae est voluptas minus voluptatem.

- followers : 2707

- following : 2943

facebook:

- url : https://facebook.com/diego.goodwin

- username : diego.goodwin

- bio : Officia perferendis enim maxime suscipit consequatur officiis suscipit.

- followers : 1220

- following : 2415